Around this time last year, the world watched as Hurricane Maria, the third hurricane to make landfall in the United States and its territories in less than a month, tore through the northeast Caribbean. In the weeks prior, in late August 2017, Hurricane Harvey made landfall in Texas and Louisiana, followed by Hurricane Irma’s landfall in Florida just a few days later. These storms cost thousands of lives (the bulk of which were lost in Puerto Rico, according to recent findings by George Washington University’s Milken Institute School of Public Health, which put the loss of life on the island at approximately 3,000 people); displaced tens of thousands of people from their homes; and caused billions of dollars in damages.

Given the possibility of a similar start to 2018’s peak hurricane season, with Hurricane Florence thrashing North Carolina as of the writing of this report, DBRS looked at the performance of commercial mortgage-backed security (CMBS) loans in the path of the most destructive of the three above-mentioned 2017 storms, Hurricane Harvey, over the past year. For a glance at the estimated damages caused by these 2017 hurricanes, refer to the table below.

Harvey Exposure

According to DBRS Viewpoint, there were approximately 1,100 loans secured by properties located in the Harvey-affected area, with a total trust balance of approximately $17.0 billion. When a natural disaster occurs, master servicers for CMBS transactions quickly identify the affected loans within their servicing portfolios using lists of Federal Emergency Management Agency–designated counties that are typically released within hours of the event, with updates made as the disaster’s full effect is assessed. Once those lists are assembled, calling campaigns begin to determine the impact on the collateral properties, and those loans secured by properties with significant damage are placed on the servicer’s watchlist for monitoring throughout the repair work. If the loan becomes delinquent or the borrower requests relief, the loan is transferred to special servicing.

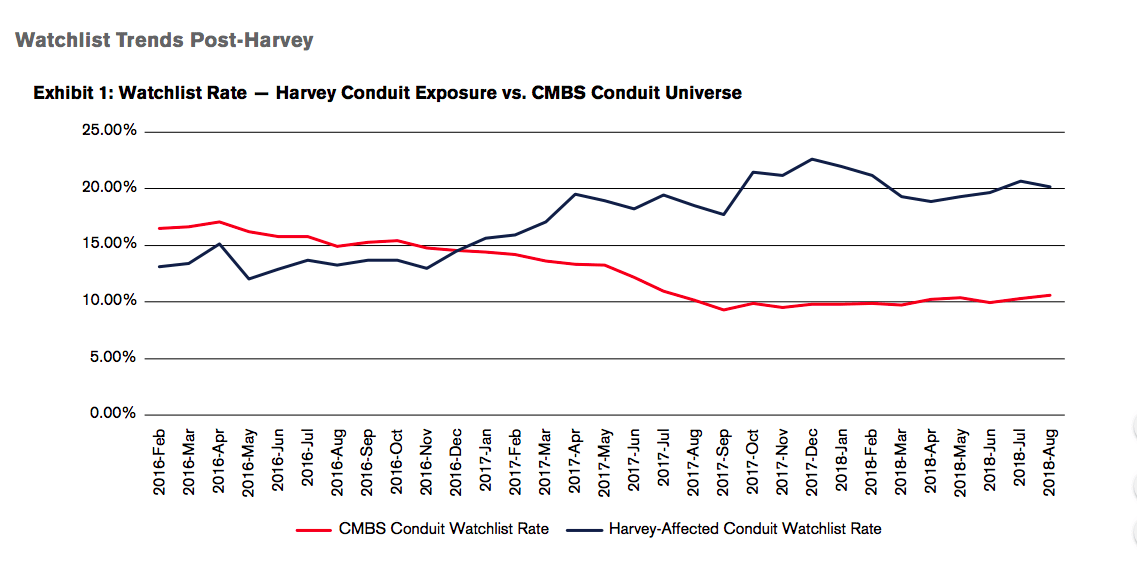

Following Harvey, the watchlist concentration in the affected areas did increase to a peak of 22.6% in December 2017 from approximately 19.5% in July 2017. Noteworthy is the fact that the watchlist concentration for the area was already quite high compared with the overall CMBS universe, which had a watchlist concentration of approximately 11.0% as of July 2017. This trend is a factor of the general difficulties within the area due to low oil prices in the years prior, particularly for office buildings and hotels. The watchlist concentration has recently fallen slightly to 20.2% as of August 2018 from the peak, suggesting some loans may have rolled off as property repairs were made and insurance proceeds were released (as applicable).

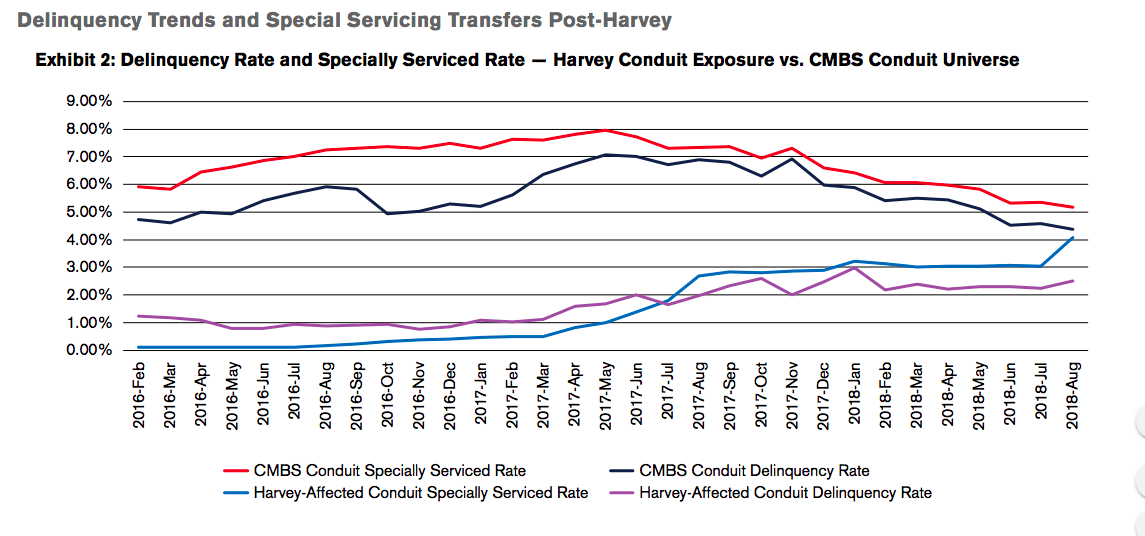

Similarly, delinquency and special servicing trends showed spikes in the months following Harvey, with delinquency creeping up slowly over the last year. As of July 2017, approximately 1.8% of loans in Harvey’s path were in special servicing, with a 1.7% delinquency rate. For the same period, approximately 7.3% of the CMBS universe was in special servicing, with a delinquency rate of 6.7%. As of August 2018, 4.1% of Harvey loans were in special servicing, with a delinquency rate of 2.5%, a figure that compared well with the overall CMBS universe’s delinquency rate of 4.4%.

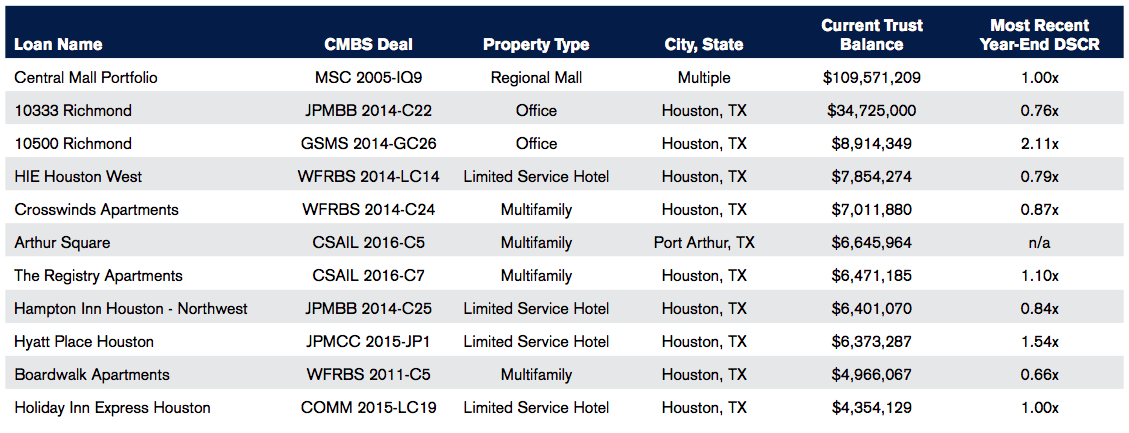

According to DBRS Viewpoint, 11 loans in Harvey’s path, with a cumulative balance of approximately $203.3 million, were new transfers to special servicing in the last year.

The largest loan transferred to special servicing in that period was the Central Mall Portfolio loan in MSC 2005-IQ9, with a trust balance of approximately $110.0 million, representing over 50.0% of the total balance of transfers. That loan is secured by three malls, one of which was located in Harvey’s path — the Central Mall in Port Arthur, Texas. Given the size of this loan, which transferred to special servicing in December 2017, it is the primary contributor to the surge in delinquency within the last year for loans affected by Hurricane Harvey. The servicer’s notes suggest the loan’s transfer was the result of the sponsor’s inability to secure replacement financing in time for the scheduled maturity. It is unclear if the Port Arthur property sustained significant damage as a result of Hurricane Harvey, but the servicer’s notes did cite lost anchors for the collateral properties as contributors to performance declines.

Just as Harvey does not appear to be the primary reason for the Central Mall loan’s transfer to special servicing, the same appears to be true for most of the other ten loans shipped to the special servicer during the last year. Most are secured by collateral located in Houston proper, with a concentration of limited-service hotels and office properties that were showing significant cash flow declines pre-Harvey and beyond. There are also several smaller multifamily loans that transferred to special servicing in the last year; based on the servicer’s most recent commentary, the only loan that appears to have been monitored for damage as a result of Hurricane Harvey prior to the transfer is the Boardwalk Apartments loan in the WFRBS 2011-C5 transaction.

Conclusions

Based on widespread reports that flood insurance was not in place for homes and businesses located in a large portion of the Harveyaffected areas, these trends are somewhat surprising. DBRS surmises the relatively low volume of CMBS loans that defaulted as a direct result of the hurricane damage in the most recent cycle (and historically) is a combination of the following factors:

- Owners of commercial real estate typically have superior resources and access to capital as compared with a typical homeowner.

- The area generally saw increased demand for multifamily properties and hotels as displaced residents sought alternative housing and as insurance adjusters, relief workers and construction workers traveled to the area to assist those affected by the storm. This likely propped up those property types in the storm’s aftermath to a certain extent.

- As residents purchased supplies and building materials and replaced belongings, retail demand likely increased significantly, incentivizing both retailers and commercial property owners alike to complete necessary repairs to allow for shopper traffic.

In general, a look at the trends does suggest the master servicers generally have effective procedures in place for identifying and monitoring those loans in affected areas, even when there are multiple events happening within a small time frame, affecting large areas in each case. In addition, historically, CMBS losses specifically tied to property losses following natural disasters have been relatively low as insurance is typically in place or property owners are able to fund, out of pocket, necessary cleanup and repair work. As development along coastlines continues to increase, however, it is likely that total damage estimates will continue to climb, as will the number of commercial structures within the path of these storms, keeping servicers particularly busy during the hurricane seasons each year.

This piece is available on the on the DBRS website and on the DBRS Viewpoint Blog.